Contents

In general, securing retirement capital in Qatar isn’t as tricky as it is in many other countries. Average salaries are above the estimated cost of living, and most residents don’t have to pay income tax on their earnings, making it easier to save. Still, planning that far in advance can be challenging. So, here’s everything you should take into account, including a mock retirement calculator you can use to determine the amount you’ll have to save.

Are you eligible for retirement in Qatar?

Qatar generally does not tax employment income, which increases residents' savings potential. The minimum retirement age in Qatar is 50 for males and 45 for women. Workers are required to serve for a period of 25 years to qualify for a pension.

Pension and social insurance plans in Qatar are only for nationals. Expats, who make up a large share of the population, plan for retirement privately. In addition, expats may need to plan for retirement both in Qatar and abroad.

Lastly, employees in Qatar are entitled to an end-of-service gratuity under Qatar labor law. This amount is calculated based on the number of years of work.

Step-by-step guide to retirement planning

Step 1: Calculate your retirement needs

The first step in retirement planning is to determine how much you will need to maintain your lifestyle and assess whether you can meet that goal with your current savings and investments. Here’s a mock retirement calculator you can use:

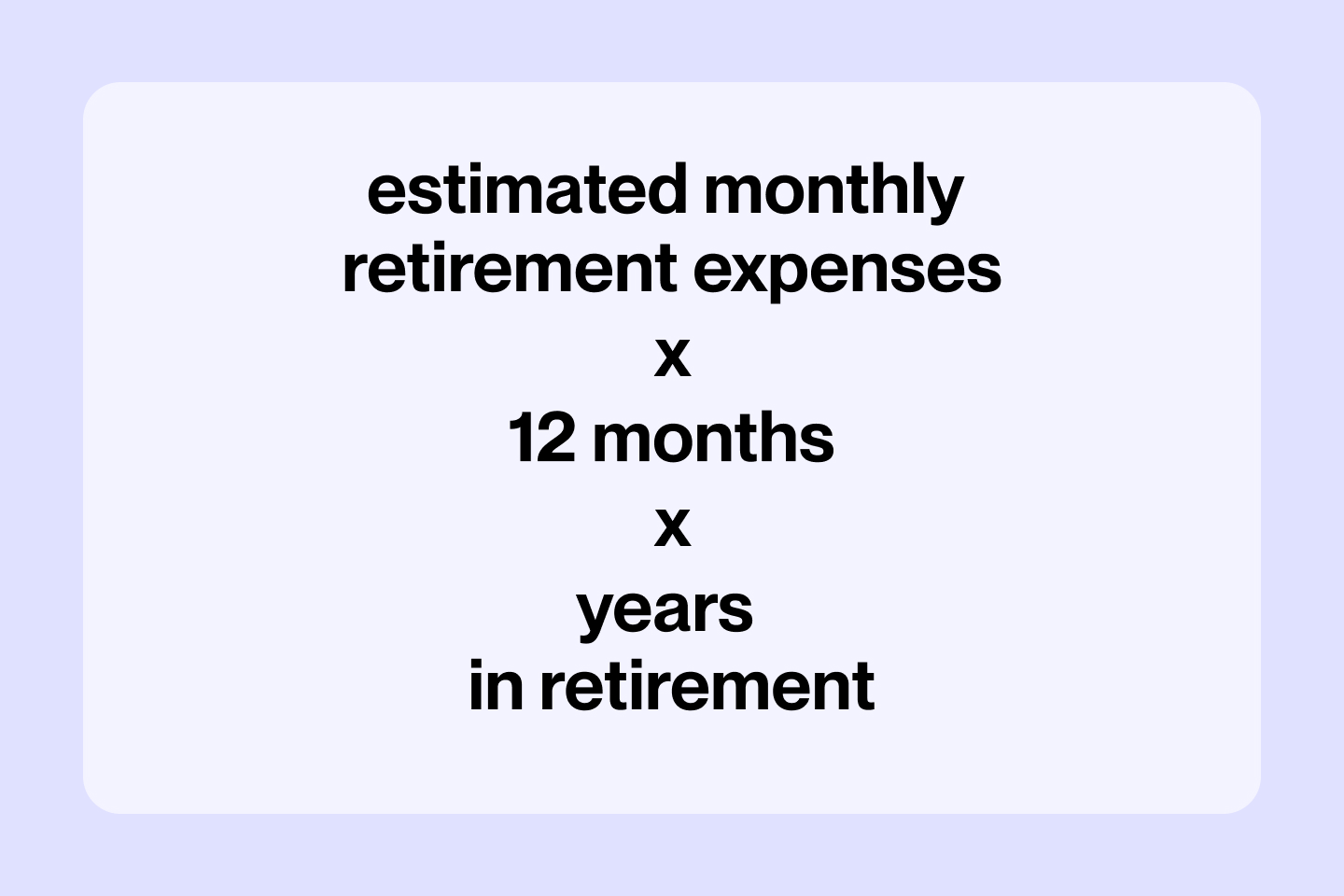

1. Estimate monthly retirement expenses.

Your retirement expenses are determined by your desired lifestyle during this period. It is highly dependent on the place where you’re planning to spend this time, as well as your leisure, travel, and family support. For instance, living in Doha means you’ll have to set aside more for housing and leisure due to the higher cost of living than in the rest of Qatar.

Also, many expats plan for regular trips abroad, which can cost QAR 15,000–30,000 each year. The financial implications of these trips, of course, lean heavily on the destination.

Let’s assume that on average, you need QAR 18,000/month.

2. Multiply by years in retirement.

If your expected retirement age is 60 and life expectancy extends to 85 years by the time you reach that age, your years in retirement amount to 25. Using this example, the calculation will be:

18,000 × 12 months × 25 years = QAR 5,400,000 (QAR 5.4 million)

3. When you factor in inflation, which was 1.23% on average in 2025, the total will come up to QAR 6.75 million.

4. Calculate your savings growth.

If you save QAR 8,000/month from age 35 to 60 (25 years) at 6% annual return, the future value will be close to QAR 6.5 million.

From this result, you’ll fall short by about QAR 250,000. You may need to save more, invest more aggressively, or adjust your lifestyle expectations.

Projection scenario

|

Scenario |

Years to retirement |

Monthly contribution (QAR) |

Assumed net annual return |

Project nest egg (QAR) |

|

Conservative |

20 |

QAR 3,000 |

3% |

QAR 1,070,000 |

|

Moderate |

25 |

QAR 4,500 |

5% |

QAR 3,420,000 |

|

Aggressive |

30 |

QAR 6,000 |

7% |

QAR 6,100,000 |

Step 2: Build a portfolio

The recommended retirement portfolio plan is a diversified approach — protect your funds against volatility by combining local assets with international exposure. Furthermore, always calculate in Qatari Riyals, but keep part of your investment in global assets for diversification.

Consider building an emergency fund equal to 6–12 months of your living expenses in a savings account. Also, real estate investments are popular among expats for their rental yields. However, be mindful of liquidity when investing.

There are multiple retirement investment vehicles that Qataris and expats alike can invest in. They include Qatar Stock Exchange (QSE) and sharia-compliant sukuk and mutual funds. You could also research real estate properties in freehold zones and offshore retirement funds.

Step 3: Choose a good pension plan

Pick a retirement plan that maximises your contribution and allows for enough flexibility to protect you from the unpredictable.

A good system secures your savings even in times when you can contribute less or not at all, and even offers coverage during unforeseen events such as serious illness, disability, and death. When you reach retirement age, you can choose whether you want to receive a lump sum, allowing you to invest your savings further, or receive your pension as a regular income.

Step 4: Maximize job benefits

Companies in Qatar have to provide end-of-service gratuity after at least one year at the workplace. The amount paid out is equivalent to three to six weeks’ pay for each year of service. Get familiar with the law and your company policy so you can estimate accumulated gratuity and negotiate more effectively.

Moreover, the Social Security law increased retirement contributions to 21%, with 7% paid by the employee and the rest by the employer. Also, those who have contributed to the retirement fund for at least 15 years may receive a housing allowance of up to QAR 6,000, easing the financial burden of this major expense.

Step 5: Review and adjust regularly

Market conditions in Qatar are very dynamic, and real estate and inflation trends may shift at any time. So, you’ll have to review your retirement plan every couple of years. This will help you stay on track with your savings rate and adjust your living costs as needed.

Mistakes to avoid when planning

First of all, you should never rely just on end-of-service gratuity. It’s paid as a lump sum, but it may only provide short-term support. This is why you need to supplement it with savings, investments, and pension plans.

Additionally, failing to account for rising living expenses and inflation can quickly deplete your retirement savings. Don’t forget to also take healthcare into account. Consider opting for private insurance or allocating a specific amount for medical expenses.

Expat retirees may still be required to pay taxes in their home country while residing in Qatar. You may run into liabilities if you fail to understand cross-border tax obligations. So, get informed before your retirement years.

Most importantly, early planning is vital because your chances of a secure retirement increase when you start on time.